Sweeping generalizations about now being a good — or at least better — time to go to law school are meaningless. What is this “law school” you speak of? The ongoing tumultuous debate concerning the state of law schools, specifically about employment outcomes, is largely divorced from a basic truth: legal education is not a monolith. That a degree from, say, Georgetown appears to have greater shorter-term value these days as Biglaw hiring begins to “crawl out of the abyss” is not good news for the students at Cooley. It’s irrelevant.

In Steven J. Harper’s recent article, The Real Moral Hazard: Law Schools Exploiting Market Dysfunction (also discussed on ATL here), he details how misguided bankruptcy policy and unlimited, indiscriminate federal student loans have isolated schools from any accountability. In laying out his case, Harper describes how law schools actually operate in distinct submarkets. He identifies three of these submarkets, each offering drastically different employment prospects for their graduates:

1. National schools

2. Regional schools

3. The “Problematic Submarket”

AI Is Reshaping Legal Practice—But Tools Aren’t The Real Differentiator.

Explore the mindset, cultural shifts, and training strategies that define the AI‑savvy lawyer, revealing why human judgment, standardized competence, and integrated learning—not technology alone—will shape the future of the profession.

By Harper’s reckoning, there are 89 law schools in that third category. Generally speaking, most graduates of the Problematics are simply not finding work as lawyers. Thirty-four of these schools place fewer than 40% of graduates in full-time, long-term jobs requiring a J.D.; 13 have placed less than one-third of their grads in FTLT-JD positions. “The differing employment prospects for new graduates should be producing different economic consequences across the law school submarkets,” Harper drily notes. Should, but don’t. The law school market defies basic principles of economics, both macro- (e.g., price and supply have increased in the face of falling demand) and micro- (e.g., the cost of a legal degree is roughly the same across all submarkets).

Almost wistfully, Harper imagines what an “unimpeded market response” would look like: the Problematics would be forced to “innovate dramatically, slash tuition, and/or close their doors.” Alas, none of that has happened. Instead the weakest schools have opened their gates ever wider and continued to jack up tuition. Harper’s prescription for this market dysfunction includes linking a law school’s eligibility for the 100% federal guarantee for its students’ loans to employment outcomes. If a school meets a fixed minimum threshold (he suggests 55%) for placing its graduates in FTLT-JD positions, then it would qualify for the full federal guarantee. Below that threshold, the percentage of the guarantee would adjust downward on a sliding scale.

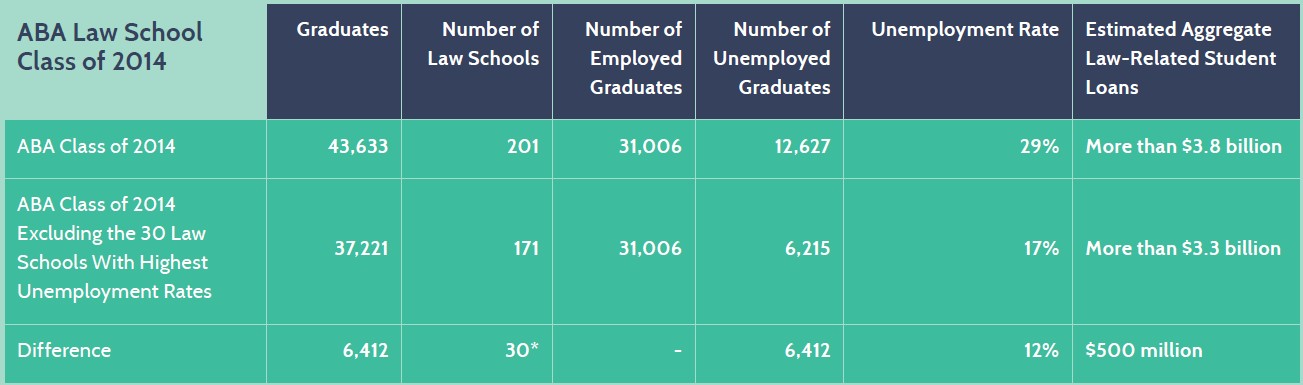

Independently, our friends at M7 Financial — who really have been on a roll lately with data on law student debt — have reached essentially the same conclusions: there ought to be a rational nexus between federal student loan guarantees and graduate employment. These dismal outcomes are not occurring in a vacuum. The Class of 2014 took out roughly $3.8 billion in student loans to finance their studies, the majority of which are government funded. This means you, dear reader (assuming you pay taxes). If unemployed or underemployed J.D.s default, it is not as if the schools will be held accountable.

The straightforward and unsentimental M7 proposal to reform the legal education market is to reduce the number of ABA-approved law schools. This is hardly a novel idea, and probably seems like common sense to most anyone who is not a law school dean. However, M7 takes the analysis a further step and quantifies its implications. M7 estimates that if the 30 law schools with the highest unemployment rates were excluded from the statistics, then the law school Class of 2014 would have an unemployment rate of 17% (way down from 29%). Moreover, the aggregate student loan burden would be reduced by an estimated $500 million (click to enlarge image):

Schenck Price Competes Smarter With Lexis+ With Protégé

LexisNexis sat down with John Ursin, Managing Partner at Schenck Price, to learn how the firm is using legal AI to strengthen client service and daily legal work.

{kind=link}

(You can download M7’s full report here.)

Without a doubt, connecting employment outcomes to federal student loan guarantees would be a huge step toward a functional legal education market. It would also force schools to improve their graduates’ outcomes (“innovate dramatically, slash tuition,” etc.) or face extinction. Is there a disinterested party who could argue that this would be a tragic thing?