With Republicans now controlling the White House, and both halves of Congress, it is highly likely that some kind of tort reform will be instituted in the next few years. Tort reform is a key plank in many Republican proposals for dealing with healthcare, and with the ACA at the top of the wish list for changes by Republicans across the board, it would not be at all surprising to see major changes to public policy in the space.

With Republicans now controlling the White House, and both halves of Congress, it is highly likely that some kind of tort reform will be instituted in the next few years. Tort reform is a key plank in many Republican proposals for dealing with healthcare, and with the ACA at the top of the wish list for changes by Republicans across the board, it would not be at all surprising to see major changes to public policy in the space.

Tort reform would have a dramatic impact on many parts of the legal industry, and I leave it to other commentators to get into specifics of positive and negative aspects of that. Instead, one interesting question that might be overlooked in such an analysis is how tort reform would impact the rapidly expanding litigation finance industry.

Let’s start by assuming that the goal of tort reform is to reduce the incidence of large lawsuits and the costliness of such lawsuits for companies. Let’s further assume that the goal is achieved by some piece of legislation. How would this impact the litigation finance field?

AI Built for Litigation. Verified by Design.

Grounded in authoritative content and verified at every step, Protégé is the only legal AI tool that delivers work you can trust—without exception.

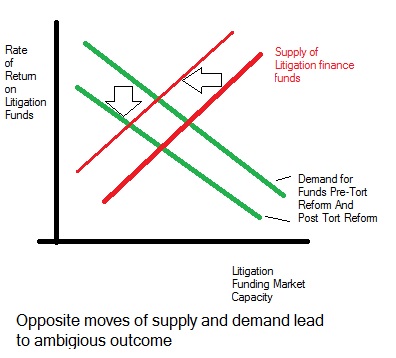

There would be two impacts in this situation. First, if tort reform makes it more difficult to bring suits – for instance, by eliminating causes of action or altering standards for class-action eligibility – it would unambiguously reduce the number of large lawsuits. That would reduce the demand for capital in the litigation financing space and hurt investors by reducing rates of return.

Second, reduced costliness of lawsuits for companies would mean that each piece of litigation was less valuable for an investor. For instance, legislation might cap payouts for particular types of cases. That would reduce the price that investors are willing to pay for new litigation claims, which in turn would equate to the same rate of return for investors.

However, there is a secondary impact here. By reducing the costliness of lawsuits for companies, it could be that firms would be less concerned with engaging behavior that would get them sued. That in turn could actually lead to more lawsuits.

Learning After Law School

Once you’ve got your law degree, how do you keep your professional skills up to date? Share your perspective in this brief survey, and you may be eligible to win a $250 gift card.

In other words, if a pre-tort reform suit would have cost a firm $1 million per product liability incident, and a post-tort reform suit costs only $500K, then a firm could afford to have twice as many failures post-tort reform.

If preventing failures is costly, then firms might well opt to have the same level of total expected legal liability exposure and simply spend less on product quality and safety. Thus the number of lawsuits would increase. That in turn would lead to more individual investment opportunities for litigation finance investors (though total investment capacity in the space would be unaffected – $1M in expected suit damages before and after tort reform, for instance).

In addition, if lawsuits become less costly for companies, that may increase interest in conventional equity investments (due to higher overall corporate products) and decrease interest in litigation finance investing (due to negative headlines and sentiment about the space). That in turn would reduce the supply of funds available for investment firms in the space, but would actually increase returns in the space as less money chased opportunities. The parallel here is in the cat bonds space, where money often flees just after a major disaster, creating higher returns for investors willing to endure the negative headlines.

It is an open question as to which effect would dominate in tort reform – the measures to make suits more difficult to bring against firms, or the decreased concern firms would show for being sued. Thus total volume in the overall litigation finance field could either rise or fall. The reality is that different industries would probably see different effects, so litigation funders specializing in particular verticals would be hurt or helped by tort reform largely based on a particular industry’s Marginal Propensity to Spend (MPS) on risk management.

All of this is speculative at this point, of course – no one knows what legislation will be proposed let alone passed next year. But for litigation finance industry participants, it is worth thinking about what the future might look like and preparing accordingly.

Michael McDonald is an assistant professor of finance at Fairfield University in Connecticut. He holds a PhD in finance. Michael consults extensively with organizations ranging from Fortune 500 companies to start-up businesses on financial matters through Morning Investments Consulting. Michael has served as an expert witness in legal disputes, and is an arbitrator with the Financial Industry National Regulatory Authority (FINRA). Michael can be reached at [email protected].